Nearly six out of ten SMEs rely on credit to buy insurance

41% of those using credit are using cards, and 35% are relying on finance from insurance and premium finance companies

The ongoing impact of COVID-19 is the main reason for borrowing more to fund credit but cashflow, rising premiums and falling business income are also factors

New research from the UK’s leading insurance premium finance company, Premium Credit, reveals that 59% of SMEs are relying on credit to pay for their insurance, borrowing on average around £1,105. Nearly one in ten (9%) SMEs who use credit to pay for their insurance, claim to have borrowed over £3,000 to fund their cover.

Premium Credit’s Insurance Index, which monitors insurance buying and how it is financed, found that of those companies using credit to pay for their insurance, 21% say they have taken on more credit over the past year for this purpose, but 24% say they have borrowed less while 37% are borrowing the same amount.

In terms of the credit being used, 41% are using credit cards, and 34% are using premium finance and/or finance provided by insurers. More than one in five (22%) have taken out personal or business loans to fund insurance while 10% have turned to friends and family for finance to pay for insurance.

Among those businesses using more credit, 43% said it is because of the ongoing impact of the COVID-19 crisis followed by 30% who said it was because their firm had taken on more credit for other reasons and did not have the cash to pay for insurance. Around 29% blamed rising premiums and 28% pointed to a drop in income. Research from October last year found 50% blamed the pandemic impact and 31% rising premiums. Figures from April 2021 were 73% and 36% respectively.

The study reveals around one in twelve (8%) who use credit to pay for their insurance have seen their premiums rise dramatically in the past year while 47% report slight increases. Just 4% have seen premiums fall. The corresponding figures from October last year are 9% reporting a dramatic increase and 47% a slight increase. Just 4% reported a drop.

In terms of the steps taken by these businesses to combat this, 20% have made cuts to their business to reduce costs, 14% say they have increased their claims excess, and 15% have reduced their level of investment in operations. Some 14% have reduced their level of insurance cover, 11% have cut salaries, and 8% have also closed parts of their business. Only one in three (32%) say they have taken no action.

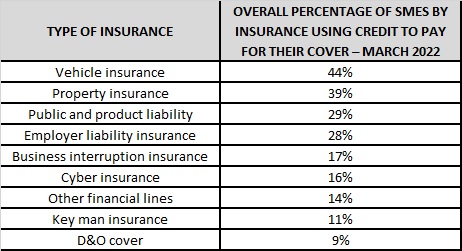

The table below shows the percentage of SMEs who use credit to buy insurance and which products they use it for.

12% of firms say they have suffered damage to property or belongings over the past five years and were unable to claim for this because they didn’t have insurance or because they were underinsured.

Owen Thomas, Chief Sales Officer at Premium Credit commented: “Credit plays a vital role in ensuring that businesses continue to have the right type and level of insurance that they need across their operations. The 100% offer of a finance option by brokers – especially because of the continuing impact of the COVID-19 pandemic on businesses up and down the country - has never been more critical.”

Premium finance companies like Premium Credit provide businesses and consumers with the ability to use a loan to pay for their insurance in monthly instalments. By managing insurance payments in this way, businesses and consumers can spread the cost of their insurance, rather than pay their premiums in one lump sum.

Authored by Premium Credit

About Premium Credit

We are the leading provider of premium finance in the UK and Ireland, and the only company endorsed by BIBA.

We are authorised and regulated by the Financial Conduct Authority, and work with over 3,000 producers of all sizes. We serve over 2.1 million customers, process 24 million direct debits and receive advances of £3.5 billion.

For over 30 years, we’ve led the market through thought leadership, innovation and technology and have helped our partners offer finance compliantly to their customers through face-to-face, telephony and online channels.

We continue to invest to ensure we provide a quality service and support that helps you grow your business and commission. From the delivery of a seamless customer journey, which includes real time decisioning for financing and 24/7 account servicing, to consultation that improves the offer of finance to customers, we are committed to growing the premium finance market.

Our Specialist Lending division also provides finance to pay other annual costs, such as professional fees, membership subscriptions, commercial service charges, golf clubs and school fees.