Pension pots of women just over half the size of men at 60-65 years old

Authored by Aviva

Latest data from Aviva has again found the gender pension gap begins to widen significantly from the age of thirty-five, and there are still significant gaps between how much women pay into their pension compared to men.

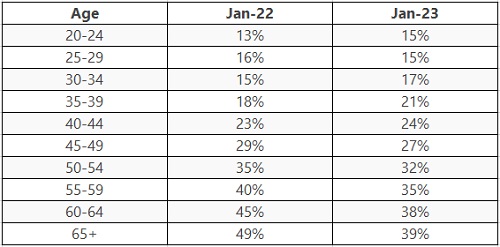

Based on the workplace pension data for just over 5 million pension plans, the gap between women’s and men’s pension contributions for 35-39-year-olds is 21%, up on the 18% gap last year. It then increases to 24% for 40-44-year-olds and 27% for 45-49-year-olds before stretching to 32% for 50-54-year-olds.

The amount paid in pension contributions has a big impact on retirement income, and the difference between women’s and men’s contribution rates is stark (Table 1).

The new data also found the gender pension imbalance persisting into retirement with women aged 60-65 years old having pension pots which are on average just over half (57%) the size of men’s pots at the same age.

Michele Golunska, Managing Director for Wealth and Advice at Aviva said:

“This suggests a clear line in the sand around the age that women are often making milestone career and childcare decisions and considering opting to work part-time . Pension contributions are unlikely to be a deciding factor when considering whether to work part-time, but what is important is that the long-term impact on a pension is understood when making that decision. This is crucial to good financial planning. Some might consider upping their pension contributions, but this would have to be carefully balanced against disposable income. An option that some parents may consider is sharing the caring responsibilities to help spread the long-term impact on pension savings.”

Aviva’s Working Lives Report (June 2022) found that women are significantly more likely to say that their workplace pension will not provide enough for them to have a comfortable retirement (40% of women versus 28% of men). It also found that part-time workers are more likely to say that they will not be able to retire comfortably on their workplace pension (46% of part-time workers versus 33% of full-time workers).

Table 1: Aviva: The gap between women and men’s pension contributions

Michele Golunska said: “It is encouraging to see the gap in contributions from age 45 has reduced, compared to last year. This might suggest there are some women who are recognising they have a gap in their pension contributions and are taking action to help reduce it.”

Measuring the gender pension gap

Aviva’s Working Lives Report also found almost one in five employers (19%) have never heard of the gender pension gap. While most employers (81%) have heard of the gender pension gap, just over two in five (41%) acknowledged they have a gender pension gap. Of those employers who said their company has a gender pension gap, 14% said they do not know the size of it.

Michele Golunska said: “There are widely varying ways in the which the gender pension gap is measured, using a host of figures which reflect household surveys of pensioners, average pension pots, contribution rates, and pension incomes. This inconsistency is a barrier to assessing progress. We would like to see the government find a suitable definition of the gender pension gap alongside a metric for measuring progress on reducing the gap.”

Remove auto-enrolment thresholds to level up pensions

Michele Golunska said: “One significant change government could make to help women and other part-time workers would be to remove the automatic-enrolment (AE) lower qualifying earnings threshold (LET), currently set at £6,240 per year. This would mean women in a pension scheme would get an employer pension contribution from the first pound they earn.

“We would like the government to put a ‘roadmap’ in place now outlining how and when it will implement changes to AE. Now, in the middle of a cost-of-living crisis, is not the time for radical change. By providing a clear ‘roadmap’ for changes to AE, government will give employers and pension savers time to plan, which will help to ensure better retirements.”

Aviva’s tips on how to reduce your pension gap:

- Make use of digital technology to help understand if you are on track for a financially comfortable retirement. Aviva’s online retirement tools My Retirement Planner and Shape My Future are free to use.

- If you are working part-time and automatically enrolled into a workplace pension scheme, consider increasing your monthly contributions, if it is affordable.

- If you earn less than £10,000 per year, speak to your employer about your options for joining your company pension scheme.

- If you are thinking about reducing your working hours to help balance family life, you might want to consider whether it is better for you or your partner to work part-time. As part of those considerations, you might want to look at which of you gets higher employer pension contributions.

- When it comes to saving into a pension, starting early allows a small contribution to build up over time.

- Long term relationship circumstances can change and should divorce become a possibility keep pensions at the forefront of your mind when splitting assets. Sharing pensions as part of a divorce or dissolution of civil partnership the same way as any other wealth does not happen by default. Aviva found one in seven people (15%) did not realise their pension could be impacted by getting divorced and a third (34%) made no claim on their former partner's pension when they divorced.

- Check your National Insurance record to see if you will get the full State Pension amount when you retire. You need a total of 35 years of National Insurance contributions, or, in some cases, you can apply for credits. If it looks like you might be short, you might have the option to pay to fill in the gaps.

- Apply for child benefit even if your overall household income means you need to pay it back through a high-income child benefit charge. If you are not working while looking after a child, you get state pension credits automatically until your youngest child is 12 years old if you are claiming child benefit. If you do not claim child benefit you do not receive the credits.

- Talk to your employer about the policies they offer. For example, Aviva offers six months’ equal parental leave irrespective of gender, alongside salary exchange. Which means employees who might only receive statutory maternity pay for part of their parental leave maintain full pension contributions.

- Seek guidance or professional advice: You can get impartial guidance on money, pensions, or debt from the government’s free MoneyHelper service. If you want personal financial advice, we recommend finding a professional financial adviser. Advisers may charge for their services, but the advice you will receive will be tailored to your individual circumstances. For those who are over 50 and considering their pension options, the government-backed Pension Wise service from MoneyHelper can provide free guidance.

About Aviva

Aviva Insurance Limited is one of the UK’s leading insurance companies, part of the Aviva group with 34 million customers Worldwide. Aviva Insurance has been in the insurance business for more than 300 years.

In UK commercial, the insurance market remains challenging for insurance brokers and customers, due to the ongoing economic conditions. Aviva Insurance are focusing on improving our processes to ensure Aviva provide commercial customers with insurance cover at an acceptable price. Insurance brokers also recognised our excellent customer service by voting us Insurance Times General Insurer of the Year in 2012, for the second year running. youTalk-insurance sharing Aviva insurance news and video.