10 ways to combat Underinsurance

Authored by Allianz

Insurance is a key purchase for businesses and getting the right amount of cover is critical for your customers. Finding out at the point of claim that cover is insufficient and that they are underinsured, can have devastating consequences.

Here are 10 things you could consider with your customers to help them avoid being underinsured.

1. Raise awareness

With the Bank of England expecting the rate of inflation to remain above 10% for the next few months - raising awareness of underinsurance and educating customers of the possible impact is more important than ever. Ensure your customers understand that if a business isn’t insured adequately then a loss may become a financial burden to the business.

2. Encourage regular property valuations

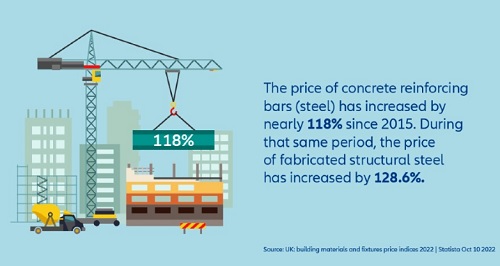

With the prices of many construction materials in the UK having increased significantly in the past year, it’s important to encourage customers to have regular professional valuations to ensure the sums insured are accurate and that additional expenses are accounted for. This is because the current inflationary levels are likely to outstrip market tolerance for sums insured, which may leave customers exposed at the point of claim.

3. Check rebuilding costs

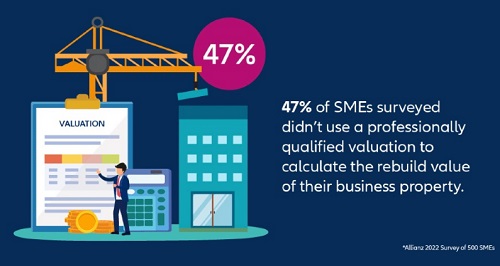

Also make sure that your customers sums insured for buildings is based on the cost of rebuilding the property and not the market value. This may include cost of materials, labour costs, professional fees and site clearance. A recent Allianz survey* showed that nearly half of SMEs didn’t use a professionally qualified valuation to calculate the rebuild value of their business property.

4. Got everything covered?

Remind your customers to include any fencing, walls, car ports and hard standing in any rebuild estimates.

5. Check the indemnity period is sufficient

When calculating indemnity periods, your customers should to bear in mind that 24 months is likely to be the minimum period needed for a business to fully recover after an event.

Our recent survey* showed that on average respondents expect it would take just over nine months to get their business back and running to its current level if their property were to incur fire damage.

When setting indemnity periods, customers need to take into account the higher energy prices, increase in material costs, current price inflation and shortage of skilled tradespeople to ensure that they are covered appropriately if things go wrong.

6. Encourage business continuity plans

Given the uncertain times many businesses have faced over the past few years, it’s important for them to regularly assess their limits of liability and develop a business continuity plan.

Creating a plan can help identify gaps in cover and identify emerging risks such as cyber, which businesses must think about.

7. Explain sums insured

With the prices of many construction materials in the UK having increased significantly in the past year, it’s important to encourage customers to have regular professional valuations to ensure the sums insured are accurate and that additional expenses are accounted for. This is because the current inflationary levels are likely to outstrip market tolerance for sums insured, which may leave customers exposed at the point of claim.

8. Are customers aware of indexation and rate strength?

Whilst both of these factors increase the cost of insurance for a customer, they’re applied for different reasons. Insurers apply rate change to reflect any changes in the cost of underwriting business from one year to the next, whereas indexation takes into account the change in the various costs associated with reinstating a business to the position they were in prior to any claims being made.

You can read more on Indexation and Rate strength here.

9. Check the value of stock

The stock sum insured should reflect the cost of the insured to replace the items, not at the retail price. When setting the sum insured, customers need to consider the maximum value at risk during seasonal or other peak trading periods.

10. New purchases

Customers should make their insurers aware of any new purchases that may impact the overall sums insured, so that they can be added to the policy. Otherwise customers may find themselves underinsured.

About Allianz

Allianz Insurance is one of the largest general insurers in the UK and part of the Allianz Group, a leading integrated financial services provider and the largest property and casualty insurer in the world.

The mission of Allianz Insurance is to be the outstanding competitor in our chosen markets by delivering products and services that our clients recommend, being a great company to work for and achieving the best combination of profit and growth. We aim to achieve this by putting the customer at the heart of everything we do.

Allianz is able to offer customers a wide range of products and services including home and motor and commercial insurance with full range of products and service for sole traders' right up to large commercial organisations.

Allianz Insurance employs over 4,500 people across a network of 20 offices in the UK and the company’s Head Office is situated in Guildford, Surrey. Our heritage and financial strength help make Allianz what it is today; a safe and trusted partner. Over 40 FTSE100 companies partner with Allianz. youTalk-insurance sharing Allianz Insurance news and video